Bargain Hunting Through Schizophrenic Highs and Lows in SGD Bonds

A new friend with a SGD 6 mio bond portfolio and we would imagine he would be sufficiently diversified with that with 20 names, all bought in 2014, a good year for bond issuance in Singapore with 153 bond issued that year. Yet he is sitting on an estimated 20% loss at the moment, with 2 names in default and the rest suffering from contingent losses in value.

Fortunately, he is a pretty good businessman in his own right and business people understand risk slightly better and know when to blame themselves for letting their bankers led them into folly although swearing never to touch a single bond here forth and I did not have the heart to tell him I was told a certain Nam Cheong bond went for some 50 cts the other day.

While most of the Singapore bond investors and press members out there are in various stages of panic and pointing the finger of blame, I note the irony of this month because the Singapore government 30Y bond hit a historic record low in yield, 3 days after Joseph Schooling won Singapore’s first Olympic gold medal, giving the bond issued in March this year about 15% returns for the year so far (price has come off about 2% since).

Market Schizophrenia

It irks me to read all these notes to their clients by the private banks about how more bonds will default in the coming months because we know that banks are abandoning their clients by the hordes these days, leaving the corporates out in the lurch as these companies need to cough up cash to face bond redemptions and Perisai Petroleum, with 125 mio due in October, announced through the SGX that they would be engaging bond holders for discussions.

Do we really need more reporters looking for their 15 minutes of fame with daily elegies on who is in trouble next, a change from writing about the real estate market?

My question is, where were they last year? When they were barking praises of the resilience of the Singapore bond market and blindly echoing the optimism of MAS as late as last December?

Image: BT

Image: ST

Only to make a drastic U-turn in March this year after the last retail bonds were issued on SGX about the moms and pops who have not been able to get a price out of their bankers and thus, have been hopelessly stuck for a long time.

A montage of U-turn articles.

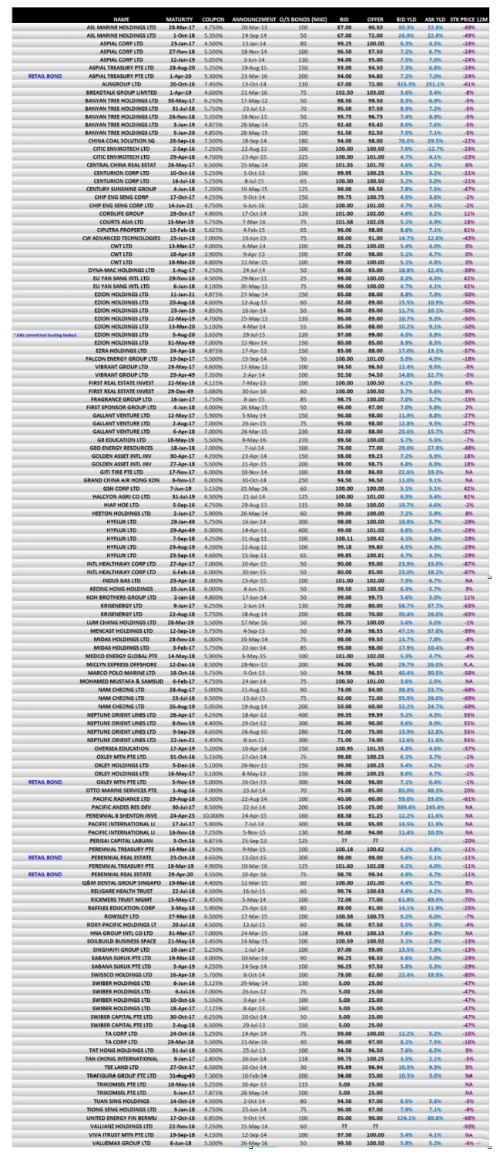

The irony lies in that there are about 130 “mom and pop” bonds out there i.e. bonds issued to mainly retail investors that have sunk in value out of our universe of just over 600 bonds in SGD dollar space and that is 20% of bond issues, although not in notional value of course, because these are invariably the small corporates that gave investors the higher yields in the days when it mattered. 20% is a lot for a country that is hoping for a bond market renaissance to save the invisible IPO market.

As investors of the 30Y government bonds rejoice along with SG 51 and Olympic gold, we find that the rest of the market hits a snag with those small bond issues offered between 2013 to 2015 are left high and dry which absolves the banks because banks are not supposed to be responsible for events that happen after 2 years or know what to expect.

It is all schizophrenia to me, as an observer, unable to digest the “hot and cold” of local market sentiments made worse by irresponsible reporting where an article alleges that Aspial bonds were going at 10% because the reporter had not verified that the bond had a few months left and probably used the bid price to arrive at the sensational yield number. At the same time I highly disappointed to learn from some investors that banks are not even willing to sell them the distressed bonds being offered out there while they were quite happy to sell them at 100 when times were good, choosing to have nothing to do with the same bonds they were marketing away then.

Yes, the new product they would be hawking would be their discretionary portfolio management product where the fund managers retain an annual management fee to keep your money safe from these nasty defaulting local bonds, or encouraging clients to buy into USD bonds instead , especially those high yield bonds that have already rallied 13% (on average) this year because they would have exit prices on the next sell off?

Let’s Be Circumspect

Some rationality is required as papers are now screaming for the government to set up something similar to the SME Assist fund they launched during the crisis (yes, SME Assist has about 5 bond issues left). Is that not akin to the “bad bank” funds we read about in Italy and gang?

I decided to “constructively” tabulate most of these “mom and pop” bonds out there that are mostly trading under their issued price i.e. 100. Throwing NOL in for good measure, because I know more than a handful of individuals invested in it, we have about 16 bio dollars worth of bonds sitting in the hands of mostly private investors with the quantum possibly lower as institutions could be vested in some of the larger local companies like NOL, Oxley, Sabana, Soilbuild just to name a few.

If each private investor is like my new friend mentioned above, with about 5-6 mio invested in SGD bonds, then we have just less than 3,000 people suffering financial loss, if any, because we do not include the coupons they have clipped/earned since their purchase.

As I write, there are astute investors on a bargain hunt this week for distressed papers and one of them could well have bought the Nam Cheong bond at a ridiculous price. We would assume they would know what they are doing which is buying when others are selling and knowing the risks involved versus their potential returns and deciding that the price is a fair one.

It is a mostly ugly table (prices unverified) although there are some bonds that are holding up which is a relative concept because any government bond, including the short dated ones, would have outperformed. The reason why some of the prices are really up in the air is because banks have long walked away from game, for instance, the Perisai bond, I was informed, have not traded in very, very long time.

I will stop short here because Perisai will be conducting their bond negotiation exercise soon and my new friend happens to be an unfortunate investor.

Schizophrenia Aside

It is all well to read those “yapping” headlines and private bank newsletters to get an idea of how much market panic they are sowing without gaining an ounce of constructive thought (except the subliminal message to buy into their latest new product or something else).

Perhaps panic is the right theme because we had Royal Industries (Indonesia) missing a loan payment on Friday as S&P reports that the global corporate default tally rose to 113 for 2016, higher than for the entire 2015 with only 2009 and its 208 defaults potentially in sight.

Speaking to a private investor who is keen on SGD distressed bonds at the moment, his comment was that besides being totally unconstructive, these headlines will not endear banks to clients any more than alienate them and it is not just the investors but the corporations that the banks are walking away from which leaves only a government bail-out as the last resort.

Gone are the days when the banks were there, stalwart, through the crises which won the hearts and minds of their investors and I recall the days of the Asian crisis where local banks maintained stability as much as they could, along with the central bank which has been silent during this market panic, leaving SGX to do the firefighting in their efforts to keep Singapore’s dream to be bond centre alive.

In our discussion, the private investor mooted crowd funding as an option and I latched on the possibility of crowd funding a distressed bond fund?

Yet with such poor market liquidity and schizophrenic markets, we do not really know the market depth for purchasing the bonds before the headlines start screaming everything will be ok again.