Singapore Rates Outlook 2017: Falling Down The Rabbit Hole

2016 Has Been A Year To Forget

So we emerged bleary eyed from 2015 into a dream state in 2016 and now to go down the rabbit hole in 2017 as we struggle to adjust to a new economic reality amidst global political change. Paradise Lost, as Singapore’s growth engines splutter and we wonder if we need a referendum to choose a side in the global political chess game?

As we had pointed out last year in our Diminished Prospects is like “Alamak, It is Buay Pai But Sian” piece, 2016 became a weary year with little to cheer about.

And so the stress levels have grown as we suggested in Eat, Pray Love—Stressed Out Singaporeans and the Singaporean Economy, Singapore took a stumble in 2016, proving all the hopeful economists wrong, as usual, with 2016 GDP looking to come in closer to 1.4% in the last survey and hospital visits are at record levels.

It is very hard to be optimistic in Singapore whose problems started back in 2015 that we recommended playing Pokemon Go in SG51 as an antidote to economic gloom. When we have less to look forward to in 2017 with economists cutting their forecasts (again) even after a Donald Trump and oil inspired rally led the STI Index to a 12 month high on 8 Dec after we saw the STI hit a 5 year low on 3 Feb this year.

5 year Daily Chart of the STI

With the growth forecast for 2016 cut to 1.4% and only expected at 1.5% for 2017 in the most recent survey of forecasters sent out late November (post Trump), Singapore companies were right to have been pessimistic beforehand chalking the lowest in a September Reuters survey with a sharp plunge in expectations.

Image source: ST

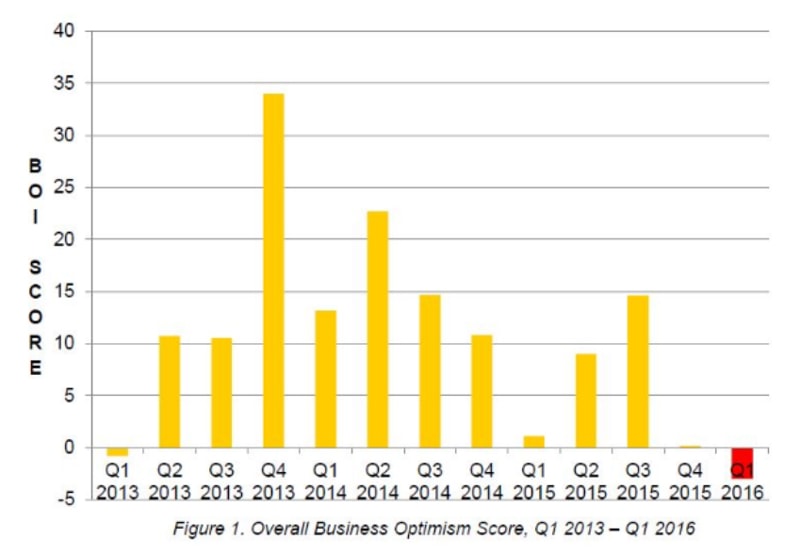

Bad news was reiterated by a historic low in a business confidence poll on 1 Dec, measuring overall business optimism since 2013.

Image source: CNA

It is not just the businesses who are feeling down, consumer confidence measured by Mastercard “indicated that Singapore ranked second-lowest on the Index in the Asia-Pacific region in terms of overall consumer confidence” for the second half of 2016.

Part of the blame would lie in the number of workers laid off in the 3 quarters of 2016 which rose to a 7 year high and its highest since the 2009 crisis with a total of 13,730 workers laid off, according to the Ministry of Manpower.

Yet Singapore is facing a shortage of talent in the tech space which is the reason why Porsches are still selling well with the government ready to spend $120 mio to fight that shortage. Yet we have to thank UBER, Grab and Deliveroo etc for providing the interim employment for the folks laid off. We do have to thank UBER for supporting those COE prices for most of the year, in time for the collapse in price this month, giving Singapore car buyers a joyous Xmas.

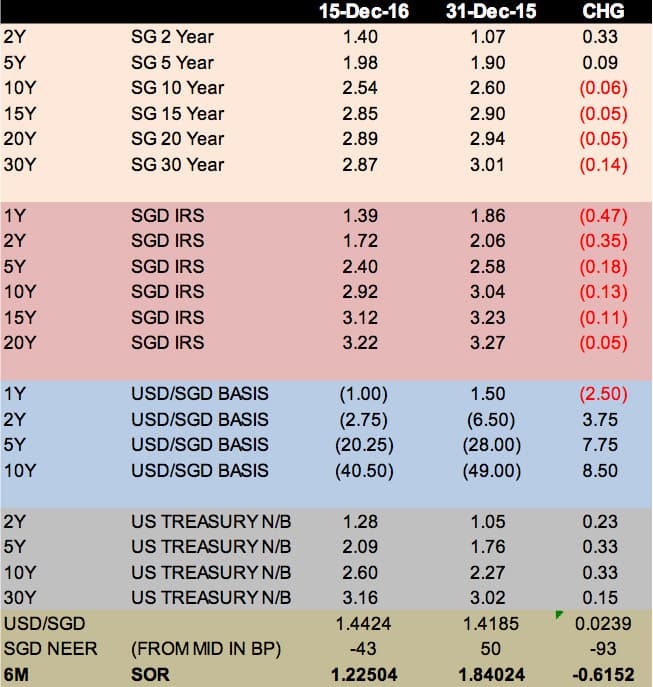

The Interest Rate and FX Wrap

Singapore government bonds have mostly outperformed the US for the year, even with the nasty sell off in the past 2 months. Interest rates have also done well compared to the rest of the Asia even with the MAS switching to a zero appreciation stance to keep the currency on the weak side as inflation continues to wane, suppressed by slower growth.

The auction calendar has been heavy with 27.8 bio worth of new bonds hitting the street for only 15 bio of maturity, all inflicting heavy losses on the buyers except for those issued in the first 2 months of 2016.

Overall, the performance has been remarkable with prices holding higher than the close of 2015 which suggests market resilience and demand despite our lack of QE, countering market weakness in other parts of the world.

The interest rate curve steepened as SOR and SIBOR rates fell in the course of the year, despite the weaker SGD in the NEER basket while basis swaps retreated, as a sign of little USD shortage onshore or demand for the greenback.

If a picture tells a thousand words, then the following chart should say it all. Note that SIBOR and SOR have not kept up with the USDSGD climb which suggests that traders and investors probably expect unexciting times ahead and for the economy to plod along un-dramatically in the medium term and shall not speculate too much in the SGD dollar, a good sign for SOR and SIBOR indeed.

5 year chart of the 6M SOR, 3M Sibor against the USDSGD

THE GDP and CPI have been sending a depressing message, in aid of the USDSGD and we note the SGD NEER Index (white line) closing the year roughly where it started, writing off the historic high in between.

20 year chart of the CPI, GDP and SGD NEER

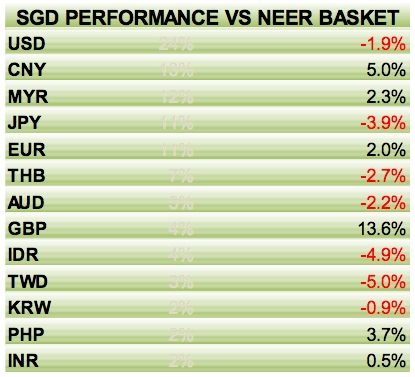

The SGD dollar had a mixed performance versus her NEER basket, gaining against her largest 2 major trading partners China and Malaysia but losing out to the US, her 3rd largest trading partner.

2017—Falling Into The Rabbit Hole

It would be imprudent to make a call on the direction of the USDSGD without making a decisive call on global sentiments or commodity prices and uncertain political developments in the west where we shall see a shaky year of market instability caused by elections in Europe and Brexit, along with the big gamble in new US President Trump.

We can only expect with certainty that the MAS will do their utmost to keep the population financially sound as they have done in 2016 that we had written about and we are lucky that the SIBOR is holding her own against the noise in the marketplace where we see 1m T-bills at >1% (vs 0.05% last year when SIBOR was at 1.2%).

The USDSGD view stands notwithstanding all those reporters calling for 1.47 or 1.5 that had relatives ringing to ask what they can do to hedge to which the reply would be, “the NEER has not changed much, if anything, perhaps the IDR or Gold”.

As we said months back which has been vindicated by the chart above of the USDSGD diverging from SIBOR rates, the NEER is in a sweet spot and there is less cause for speculation of further weakness versus the rest of the world even with the USDSGD at a 6 year high now, from its last 6 year high in January 2016.

Yes 1.47 or 1.5, if we see China devalue again or the some massive risk-off hits the region, but the SGD dollar should hold its own in the meantime and perhaps even gain some momentum from safe haven flows in the months ahead.

8 year chart of the USDSGD

SIBOR and SOR would probably continue to lag any further gains in LIBOR, to remain capped as the authorities keep liquidity in the system flushed like they have been for 2016, managing liquidity and forex separately.

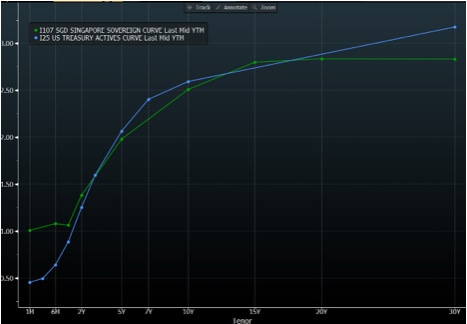

Singapore bonds should, therefore, continue to buck the trend, finally turning the tables on the US after 2 long years of languishing in the higher yield domain, a new record. A feat that has paid off as 10Y SGD govies close the year under US treasuries.

Now, SGD yields mostly below US yields

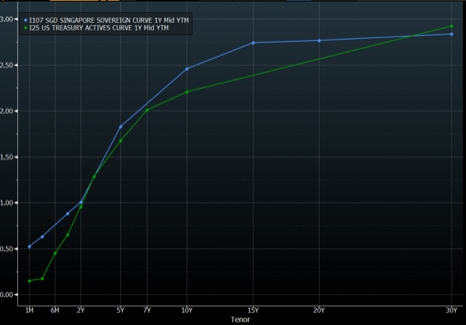

1 year ago, SGD yields above US yields

We have a light auction calendar ahead for 2017 with only 1 new bond issue and 2 extra 1 year bill auctions, it would be easy to suppose that it would be a long-bond friendly year with the caveat that the demand and supply picture could be balanced by cyclical rotations into other asset classes or extra supply stemming from the corporate bond market (which we will discuss about another day).

Bond issuance calendar 2017

A Final Word

Global economic and political uncertainty will obviously play the bigger part in the shape of the yield curves but the risk for Singapore is positive in the partisan waters of the region. That is Singapore’s joker card to play which carries a potential windfall from parties looking for a harmless place to do business or to relocate to, given the government’s efforts to promote the fintech market and emphasis on technology, research, workforce retraining and more.

The 2nd anniversary of Smart Nation Singapore has passed us and Singapore could be at a turning point to garner some attention as a tech centre. Just speculation, of course, with sentiments at ground level still bordering on despair and ordinary folks stress out of worry on their jobs and stagnant wages, prospects looking even more diminished than 2016.

It would be a waste of time thinking of the dire possibilities of 2017 and the inevitabilities that we face in terms of market volatility. Like falling down a rabbit hole, we cannot know what to expect but like Alice said, “It’s no use going back to yesterday, because I was a different person then.”