Happy Horrors for Halloween: Singapore Corporate Bonds Have Outperformed

– October comes to a roaring ending with a new high in stocks and a new en bloc as each week passes.

– With the S&P set to match the record of 12 consecutive Up months (2 days left), Singapore’s imports of Swiss luxury watches spike 90%

– Meanwhile SPH grapples problems with costs and decides to shut down the Asiaone website in a world where journalism would not be typical sensible career choice

– Singapore news will never be the same but we will beat the Straits Times to it when we say that Singapore’s corporate bonds Have Done Well this month

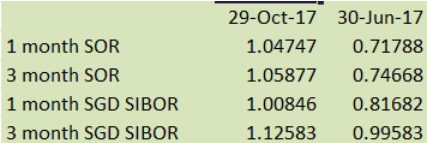

– Despite heavy selling in the government bond market has left prices 0.5 to 1.6% lower across the board and down 1 to 3% since end June with interest rates up some 0.25% across the board led by SIBOR and SOR

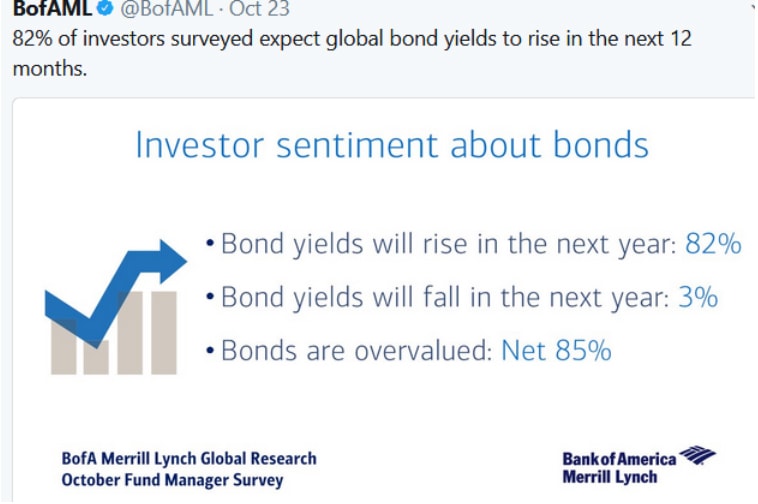

– 85% of professional respondents in BofAML client survey sees bonds overvalued as central banks prepare to hike rates or cut their stimulus packages or both which more or less sets the course for higher rates in time to come

– However Singapore corporate bonds are doing extremely well with most registering healthy price gains or negligible prices losses.

– We could postulate that investors here are behind the curve and some may even be unaware that interest rates have increased this month which is not surprising given the lack of publicly available information

– It is still a puzzle to some so-called experts as to why most Singapore corporate bond prices have not changed in the past month when we had a meaningful correction in the government and HDB bonds

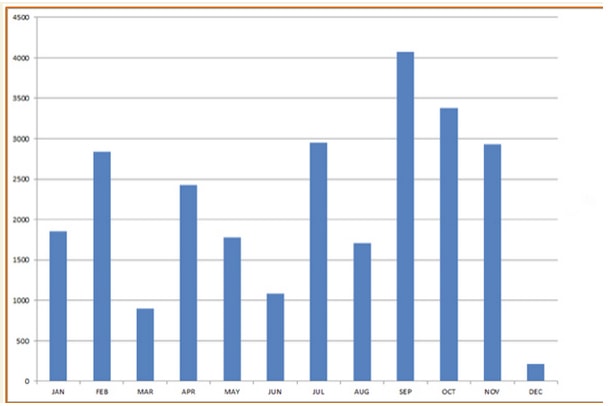

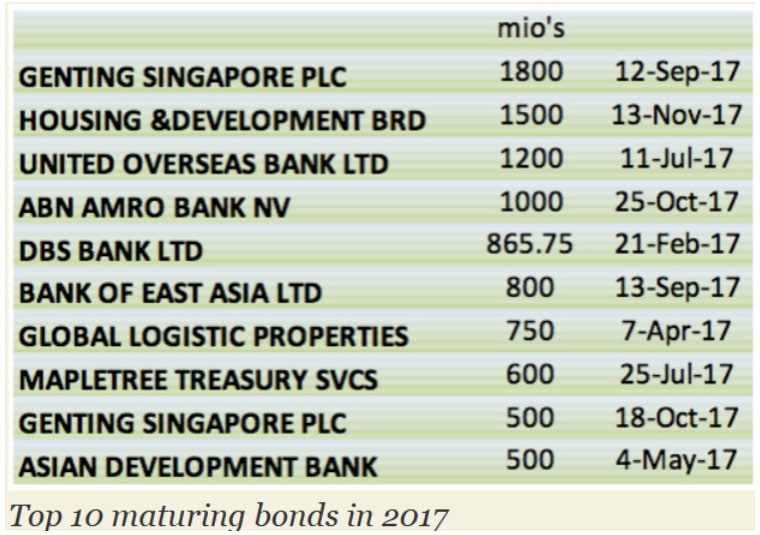

– The answer could be as simple as what we said in our 2017 outlook, that Sept-Nov 2017 stand out as the months with the heaviest maturities and maturities of retail-staple bonds such as Genting. Retail investors are typically less sensitive to interest rate moves

– In additional global HY spreads have tightened to their pre-Lehman lows

– Puzzle solved although smart folks would sell those bonds whose prices are unchanged to buy bonds that have cheapened

– It is a happy horror story for Halloween so far – that Singapore corporate bonds have outperformed – until we realise that bonds are Not non-renewable assets with supply aplenty as 2017 has proved to be a record-breaking year for issuance in Asia

Happy Halloween

Finding it hard to adjust to the new reality where markets make a new high to close each week and not a week goes by in Singapore without another en bloc sale?

You are not alone as October 2017 roars to its end with most traders smiling broadly because volatility rocks, cash tills ringing.

Is it any wonder that Singapore’s imports of Swiss luxury watches spike 90% in September, making Singapore the 3rd largest importer of luxury timepieces? (Or perhaps the Chinese are just too afraid to buy them at home?)

Source: Business Times

Everybody is getting into the new swing of things as gym instructors talk about Bitcoin and taxi drivers tell us that interest rates are heading higher. Every other folk we come across appears to be wondering if it is time to enter into a property investment as our weekly en bloc windfall goes to Crystal Tower on Ewe Boon Road in Bukit Timah, netting each owner between 4.6 to 5 million dollars. It has indeed served them well for not their original decision not to build to the max of their plot ratio because people were just not that greedy in the past?

Even the URA dampener “seeking detailed information on the tender results of private-sector en bloc sales from marketing agents, including the names of all bidders and their bid prices”, will not dent sentiments nor the URA data released on Friday that future homes from these en bloc’s and land sales could nearly double the number of private residential units in the pipeline.

Wealth is created daily with every single new floor we add to the country in terms of valuation and the financial leverage that it allows. What are you waiting for? Borrow away!

Yes, there is a mad grab attitude right now just because America has opened the spigot of budget deficits and a tax plan that gives markets a lot to anticipate in the logical or illogical reason for stock buybacks at record highs?

Who cares because it will be a new high next week despite closing this one on a dicey doji candlestick pattern? Or perhaps not because US President Trump will be in China and deprived of Twitter, Facebook, Youtube, Google, Yahoo, Instagram, Pinterest, NY Times and God Almighty, Bloomberg too!

12 consecutive up months for the S&P 500 matches the longest winning streak in history and we just have 2 days to go.

Source: Twitter

It shall be Happy Horrors for Halloween this year!

Singapore News Will Never Be The Same

It is a shame about the Asiaone website which will shut down after 2 decades in our lives.

News will not be same for a lot of Singaporeans again without Asiaone. Lucky we weaned ourselves off sometime in April this year after their garish Snapchat colour-themed polka dot facelift that just didn’t do it for our poor eyes.

While the SPH management has been seen as unapologetic in its recent cost-cutting (= retrenchment) exercise, shareholder value will no doubt be boosted in times when journalism would not be a sensible career choice in the world of fake news and presidents against the media.

It does not take a lot of imagination to see why some say the quality of local journalism has fallen just as local economists are herded to only making the “shiny happy people” optimistic calls.

We are not in a position to judge and this is definitely not a bash session, but, for once, we will beat the Straits Times to it when we say that Singapore corporate bonds are doing well this round but we do not think that this is a sustainable trend.

We will not make the obvious lame duck statements from Bloomberg like, “Clifford Chance Says Spike in SGD Bond Defaults Unlikely in 2017”. Seriously, for lack of things to write about?

Source: Bloomberg

Yet we are pretty used to misleading headlines like these that got us all excited back in 2015 before the flood of defaults began.

Source: Business Times

Source: Straits Times

What We Mean About Interest Rates Going Up

We will start with the interest rate market.

Singapore interest rates have come off a lot in 2017 with government bond prices up 0.5 to 3% since Jan 2017.

Yet, in the past month, heavy selling in the government bond market has left prices 0.5 to 1.6% lower across the board. Going back to end Jun 2017, prices have come off 1 to 3% as the interest rate curve rose some 0.25% quite evenly across.

Funding rates in the 1M and 3M Sibor and SOR have also risen in tandem.

It does look like a definite trend here because, as we speak, most central banks, except for those in developing countries, are looking at hiking rates and, or, reducing their monetary stimulus. Throw in the demand for cash from the good news of the week, the soon to balloon US budget deficit that needs to be funded, and the ECB and the Fed to scale back on their monetary stimulus just to name a few factors, the trend for higher interest rates looks set firmly on course.

Institutional investors are not blind to the prospects, echoing their sentiments in the latest BofAML survey where 85% saw bonds as overvalued, a view shared by Ray Dalio, founder of the largest hedge fund in the world, Bridgewater.

Source: BofAML

Just Strange Market Dynamics?

Singapore corporate bonds are doing extremely well, nonetheless. Most registering healthy price gains or negligible prices losses.

Yet it is not unusual for the Singapore corporate bond market to be behind the curve from past experience as evidenced in the headlines above out of the Straits Times just months before the market saw its first ever local default back in 2015.

Given the lack of available information on interest rates, local and global, it would not be too surprising if some investors are unaware of swings in interest rates for the past month.

Thus it is perfectly normal for ESR-Reit to come out on Wednesday to issue a subordinated perpetual bond at 4.6% after an initial price guidance of 4.75%. This comes just 5 days after Moody’s downgraded the company’s outlook to negative while affirming their Baa3 senior(not sub or perp) bond rating. The bond price is holding near issuance levels, just 0.25% lower at 99.75, exactly where its price would be after including the private bank sales inducement fee of 25 cts.

Not so lucky would be the last buyers of Wingtai 4.35% senior perpetual who bought the bond at 101.35 days before the issue was reopened at 100 on Thursday excluding the private bank sales inducement fee of 25cts.

Strange market dynamics, I was informed by market insiders baffled that bond prices have remained unchanged throughout the market despite the meaningful correction in government bonds.

Not all bonds were spared, naturally, with HDB bonds taking the biggest hit, underperforming the government papers and with yields rising most severely in the shorter dates as higher Sibor and SOR rates took a heavy toll on their prices.

Why Are Bond Prices Unchanged Then?

If we take a closer look at the bonds and their prices, we would notice that most bonds issued in 2017 have been immune to this round of higher interest rates with the exception of the Wingtai perpetual because the issue was re-opened and, of course, those stat board papers which are closely tied to government bond prices. As for the rest, the prices losses have been miniscule, as if interest rates have been stable.

The list of losers.

Table of bonds issued in 2017 with price losses for the month of October

More meaningful would be the list of bonds which actually saw their prices pick up in a month where interest rates have risen 0.1-0.15%.

Table of bonds issued in 2017 with price gains for the month of October, leaving out those with unchanged prices

Majority of our corporate bonds have outperformed this month.

If we get down to thinking about it, there is no tomfoolery at work here and the experts are wrong to be baffled at all because if we go back to the start of the year when we wrote about the wall of maturities in 2017, September – November stick out as the months with the heaviest maturities.

Maturity ladder of 2017, unverified for accuracy, published in Singapore Corporate Bonds 2017 – No Rain, No Rainbow

We were wrong about the lacklustre demand when we said: “We do not see a whole lot of wealth generated from the real estate segment, the former lynchpin of new retail monies”. Look what we have this year – en blocs’!

As we pointed listed the chunk maturities of 2017 at the start of this year, we did not realise then that the chunk of the maturing bonds in Sep-Oct are the retail staples—the Genting perpetuals’ and the ABN Amro sub debt.

The October market’s outperformance just serves to demonstrate that retail investors are the least sensitive to interest rates and are probably behind the stable and unchanged bond prices.

The other more obvious reason would be that global corporate bonds have generally outperformed this month and that the High Yield segment has rallied to pre-Lehman lows by some 0.13-0.15% in October alone while better credit spreads have improved 0.02-0.05%. While it is hard to reconcile bonds like SIA as a High Yield, it is still a plausible excuse.

Graph of Global HY Credit Spread currently at 3.37%

Happy Horror Story for Halloween

Puzzle solved for the time being and a caution to those who would dare to challenge the power of the Singapore bond market. It is just as well that it is impossible to short sell Singapore bonds however tempting it is, although smart folks do sell out of those bonds whose prices have not changed to buy into those whose prices have.

It is a happy horror story until you realise that a bond, unlike oil and gold, is not a non-renewable resource. In fact, Jan-Sep 2017 has been a new record level of issuance for Asian high-yield bonds, according to Moody’s. Happy horrors so far with the nice rally we have seen for 2017 and the price immunity so far for October as we head into Halloween.

Like we said, it is sad to see Asiaone leave our lives but we will continue to try and value-add in the name of good journalism when we say we are not sure if the trend will sustain and SGD corporate bonds will continue to outperform for the rest of the year.

Some food for thought as we celebrate a fantastic October and the happy horrors we are dealing with on Halloween.