Good Oil Hunting

A chat with my broker friends has given me this idea to write about oil and oil stocks. I have been busy trading the oil story too, riding the Sembcorp Marine proxy before last Friday’s dip in oil prices finally despite the initial euphoria after the ECB’s massive liquidity injection announcement.

My futures broker friends say they have been getting calls from stockbrokers inquiring on behalf of clients on how to invest in oil futures and stockbrokers telling me that customers in Singapore have little choice in oil plays with really only 3 main stocks to consider – Keppel, Sembcorp Marine and Ezion (of all things?).

The rest of the small to medium sized oil related companies are generally not good proxies as far as investors are concerned, being the favourites of the stock punting world.

Futures volumes in NYMEX Brent contracts surpass 200k daily trading volume for the first time ever with 2015 averaging daily volumes of 152k vs 50k this time last year, according to CME Group. A clear sign indeed that speculators are getting involved.

Yet the month of January has only brought on bad news as the oil price collapse since June last year brings drillers to shutter their rigs and cut jobs across led by Baker Hughes (6,000) and Schlumberger (9,000) as BHP cut their shale rigs to reduce cost and keep dividends.

Examining oil price performance so far.

And the performance of Big Oil is hardly affected.

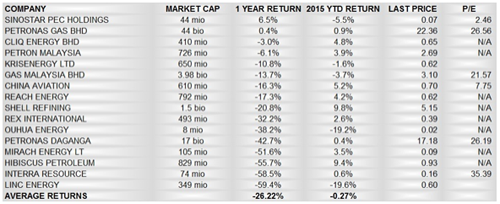

Singapore and Malaysia oil and gas companies mostly underperformed.

Singapore and Malaysian oil and gas companies ranked by 1 year returns

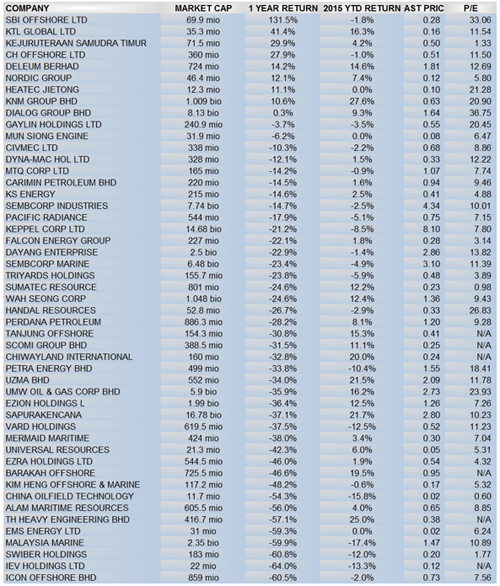

And the oil and gas services companies look none the better for wear.

Singapore and Malaysian oil and gas services companies ranked by 1 year returns

That investment decision gets complicated when we consider the oil ETFs where there are 2 types – direct commodity exposure or commodity company exposures.

Commodity ETFs ranked by total assets

Commodity companies ETFs ranked by total assets and worst performers

Observations:

- Big oil is hardly affected by the 50% oil price slide.

- Small oil is affected to larger extents.

- Within oil services, we note that infrastructure is the most resilient, delivering positive returns as noted in the ETF performance.

- Oil and gas services companies have suffered bigger losses than the oil price decline although the industry as a whole is better buffered from the oil price drop than local oil stocks.

- Oil index ETFs holding big oil companies have lost money because of the smaller oil names in the index that have affected returns.

- The pure commodity ETFs have suffered larger losses than the Index funds.

To make that investment decision, we should consider several factors.

1. Oil Price Outlook and Expectations

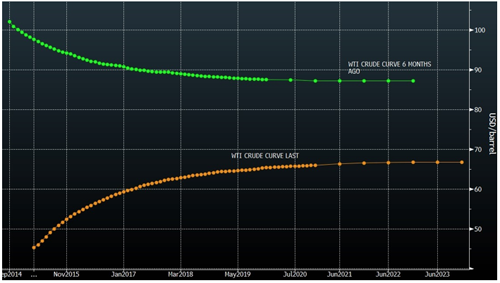

Noting that the oil curve is in contango where future prices are higher than current March 2015 delivery prices which is leading to major oil traders hiring super tankers to store oil instead of selling at current prices.

I have pointed out in a part article that oil prices have not plunged 3 quarters in succession since 2003. Forecasters are calling for prices to edge higher into the year and the recent Chinese Academy of Sciences forecast was for oil to average US$ 72 for the year.

2. Personal Risk Appetite

Oil futures are highly leveraged products. 1 contract of WTI is US$ 45,590 in value (1,000 barrels) which is traded on margin accounts and thus the smaller price swings will lead to larger profits and losses. Active risk monitoring is necessary. Oil futures are also deliverable with an option to cash settle on expiry. Near dated futures contracts have to be rolled forward unless settlement is desired. Leveraged ETFs present higher risks as well, e.g. DIG US which is a doubled leveraged product.

3. Industry Segment and Stock Selection

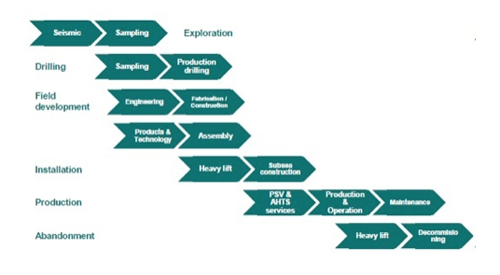

Buying an ETF would appear to be a safer option because it saves the need to identify industry segment right down to individual stocks. My personal experience has been that ETFs are slow to show profits yet now realise that they do not mete out the full loss as well. Identifying the segment of the supply chain is just the beginning.

Oil Supply Chain taken from DNB

My view from last year is unchanged. “The large resource companies will bear the least brunt from the “supply shock” 25% drop in oil prices this year. That is not to say that the smaller and less established companies will not suffer because 1. they do not hedge their prices ahead and sell in the spot market, 2. they do not have the economies of scale in operation, 3. they do not have diversified cashflows and, 4. newer companies are usually more highly leveraged and run on negative cashflows to maximise their returns. This is applicable to all the companies in the oil supply chain and the biggest risk has yet to bite them which has been their happy go lucky and trigger happy over investments in the past 2-3 years.”

Big Oil has hedged themselves safely for oil prices for 12-18 months which means they should be safe for the first half of 2015 at least. The rig orders are also placed in advance with most deliveries due in 2015-2016 following which the orders have tapered off.

Conclusion

Make no mistake, the lower oil price regime is likely to stay till 2020 and beyond. The pain for oil related companies, especially the service segment, has not even started yet but it does not mean oil prices will not correct higher from here in the future.

It would pay off to play it from the commodity angle on a short term investment horizon using for example CRUD LN, USO US and OIL US, although Singapore retail market will continue to use the proxies in the Keppel’s and Sembcorp Marine’s. The other perspective would be to play off the potential takeover targets because mergers and acquisitions will heat up, especially for pipeline and infrastructure assets which is evident in the outperformance of those ETFs.

My premise for trading oil from the long side in small short term trades is because there is a glaring absence of risk premiums built into the current prices for the events of geopolitical instabilities.

That is for the Chinese new year ang pows. As for the pocket money, we stick to Sembcorp Marine.