Demystifying The Financial Anomaly: Shortage of USD and Basis Swaps

I have been perplexed reading about the USD shortages in the negative rate world because the DXY (USD) Index has not gained in the year which means there couldn’t be that much demand for the currency.

Why should there be a shortage of USD in Japan when the USDJPY is at its 3 year lows?

Let’s demystify what is happening, using Japan as an example.

Folks living in a negative rate regime with central bankers telling them that rates will only get more negative run out of sensible assets to buy for their portfolios thus turning to USD assets which they swap back into Yen, for instance, which hedges their currency risk.

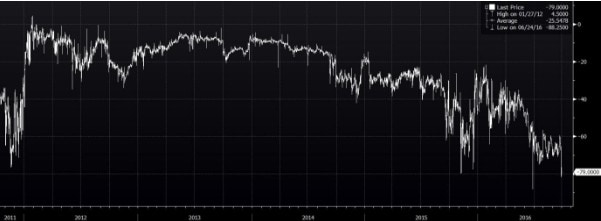

By doing that, they are effectively borrowing USD instead of buying it. This creates a demand for USD which leads to a premium for the USD that is expressed in the USD vs JPY currency basis swap which has gapped to huge 0.79% in the 3M tenor for the “borrower” or seller of the swap, effectively costing 1.64% to borrow USD for 3 months vs actual 3M Libor at 0.85%.

USDJPY 3M Basis Curve over 5 years (note –ve indicates a premium paid for the USD and the more –ve, the higher the premium)

In fact, the entire USD-JPY basis curve from 3 months to 30 years is trading between premiums of 0.5 to 0.8%.

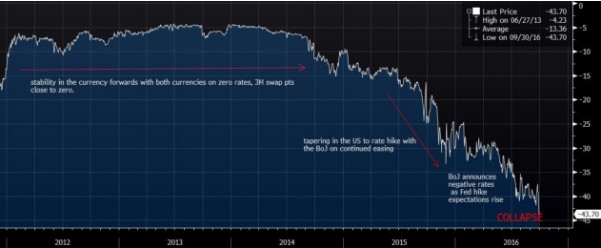

Now, a currency basis swap does not end its life there because the “buyer” of the swap has to square off his risk as well at each fixing leg, in this case quarterly, by borrowing USD and lending JPY which has led to a collapse in the USDJPY currency forwards, mimicking the basis swaps, because of the interest rate difference between the 2, exacerbated by the premium for USD.

One thing leads to another because the overwhelming demand for USD borrowing would lead to excessive selling in the forwards and we can more easily visualize it as a Japanese bond investor who receives a regular USD coupon from his USD bond that he sells in exchange for JPY.

Voila, currency strengthens despite the demand for USD because the demand is to borrow and not to buy! When you cannot buy, you buy-sell (borrow).

Sidetracking Into Basis Swaps

Now, while many of us would be stumped by the buy-sell’s and basis quotes of -0.5/-0.7, there are others who make a living out of it and fortunately, perhaps 90% of the real world does not care.

What is a basis? A basis is a beautiful financial concept that is used to apply a numerical value (and therefore being able to trade it) to a discrepancy or to what at first can seem an anomaly. As far as curve construction is concerned, a basis is extremely important as it appears to indicate where two floating rates, which we would have assumed are equal, are in fact different. Within the same currency, a basis is traded through tenor basis swaps and between two currencies through (cross) currency basis swaps. I personally hated it as much as it confused me because there is no way in the universe to explicably price what it is worth and we will not find many textbooks devoting a lot of time to this financial anomaly.

A good friend and mentor with multiple Ivy League masters degrees taught me this at a young age—basis exists and there is no way you can devise a pricing model for it except for the principles of demand and supply.

Great news, is it not?

Another dear friend tells me she once priced a 25 year USD-SGD basis trade, under severe duress, for an important client and never got out of it alive as it continues to pay the client their Libor plus 0.7% in exchange for their paying SOR (Swap offered rate) enriching the client considerably more considering that they initiated the trade when USDSGD was at 1.25, or thereabouts, making the SGD payments even more serviceable these days at 1.35 as complicated as it sounds.

Basis Awareness

The good thing about basis swaps in general is that we can live a happier life without knowing about its existence because many of us already find semi-annual bond yields hard enough to comprehend. And it would be mysterious enough for one to even start to access any information about them because there are no indices or publicly available information on them. Even if we availed ourselves to the data, there is no way for an individual to transact directly unless we have ISDA (International Swaps and Derivatives Association) agreements signed with banks that agree to provide prices to us.

The bad thing about basis swaps is that they are gaining in importance these days with financial markets frozen over. There is even a basis swap for the LCH and CME clearing houses, meaning that one pays a premium for choosing to clear with one over the other on exactly the same instrument due to collateral and margin preferences that is quite beyond me.

It is getting difficult to trade currencies without being aware of bases and you will definitely be misled by your banker if they tell you to buy a 5 year USD bond because it pays Libor plus 1% over a similar SGD bond that pays SOR plus 1%.

I would pick the SGD bond because there are the 2 bases to be aware of.

- Tenor Basis. Libor plus 1%, usually means 3M Libor and reference SOR is 6M. The 3 versus 6 month basis in USD is about 0.2% for 5 years.

- Cross Currency Basis. The USD-SGD basis in the 5 years is 0.2%.

Therefore, 3M Libor plus 1% works out to be just 6M SOR plus 0.6%. That is lesson in relative value that can be frustrating for those who know against the majority who does not care.

Imagine a sales pitch like this one – One pays negative EUR 3M Euribor (-0.3%) and receives USD 3M Libor (0.85%) for the next 3 years ? Sounds too good to be true for the unsuspecting client?

Because if we go by market levels, it should be pay Euribor at -0.3% and receive 3M Libor + 0.4% = 1.25%! That is even better, is it not?

Back To The USD Shortage Story

If the world has been rushing onto this borrow USD trade for the past 9 months after the BoJ went on rampage in January, intensifying the pace in the past 3 months due to Money Market Fund reforms scheduled to hit the US on 14 October 2016, we are moving into a period of presumed tapering of sorts as the ECB and BoJ temper their actions, if I had sold JPY basis at -0.2% and it is at -0.7% now, my worries easing slightly, would I not be tempted to take some money off the table into the 4th quarter?

Unfortunately, going by warped logic from what we wrote about earlier, wouldn’t that mean that the USD shortage has eased and thus, it will strengthen against the JPY, for instance? And we will find the USD strengthening back, on the bizarre lack of demand?