Market Thoughts: Nothing but Inflation on Our Minds

With many rushing to book the next flight out of Singapore and some already relishing the truffle season in Italy, we wonder if we can possibly endure the 12-hour flight masked up. Some people have it easier as far as masks are concerned like a dear friend’s son with his high-bridged nose while she complained about feeling like a steamed char siew bun (with the mask on) for the entire day in the office.

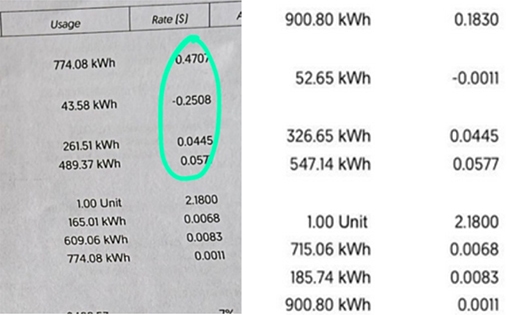

Yet the office would be the better place to be not just for the free coffee and plumbing, but the free aircon because we are properly floored by the electricity bill and lost for words, up more than 150 per cent for the foolhardy folks still sticking with the wholesale electricity market where tariffs just shot up to 47cts (+161 per cent) per kWh from just 18cts in September (refer to screenshot below). Let’s all go back to the office!

It makes us wonder how much it would cost to charge the best-selling car in Singapore for September, the Tesla, now?

At the same time, we also come to realise that the friend with the $600 bill would be paying nearly a thousand dollars more this month, which means he would need to squeeze about 0.25 per cent more returns per annum on his $5 million in retirement savings to make up for it. Assuming we all do not rush to bankrupt electricity re-seller Geneco that is still offering packages at 25cts per kWh because someone will have to pay the price for it.

But what about that block of cheese at Cold Storage that is suddenly costing $20-22 from $14 last month? And our favourite pao fan which has shrunk in proportion, now dishing out just two clams from three last month and five in August? As we read about crab shortages in America, our friends who do their household marketing in wet markets are complaining about the rising prices of fresh fish, meat and vegetables.

It is too soon for folks on fixed price plans to feel the pinch of the electricity bills (or until they recontract) but it is surely filtering into the system because it was just 10cts per kWh in June before its spike to 17cts (+70 per cent) in July before backing down to 12cts in August and up to 18cts in September for its 47cts homerun in October. We would shudder for the businesses and factories affected and wonder about the repercussions to come.

Inflation is top of almost everyone’s minds now. From the cover of Businessweek to the FT, to Bank of America’s credit investor survey to economic data, which is directly affecting US President Biden’s approval ratings as major central banks doggedly cling to their “inflation is transitory” narratives and losing loads of credibility as markets price in breakeven inflation rates at record highs.

In the past week, we had China’s PPI climb 13.5 per cent YoY, hitting the fastest pace in 26 years, a 6.2 per cent increase in US consumer prices over the last year, which is the highest rate of inflation we’ve seen in over 30 years. Japan’s wholesale inflation hit a 40-year high as fuel costs spike, US consumer sentiment fell to the lowest since 2011 as 9 out of 10 Americans worry about inflation with half looking to reduce dining out.

It is showing up in surging electricity bills in Europe (and for some people in Singapore), grocery bills, new and used car prices which are inflating insurance claims (hence premiums), apartment rents in Manhattan climbed by the most on record (up 18 per cent), coffee prices and more as retailers, corporations and landlords pass the costs along.

That is for daily life but let us not get to asset inflation which is not in the CPI basket, with runaway property prices, stock markets—with the US stock market worth just $27 trillion 20 months ago and doubling to $54 trillion today or even that Rolex Oyster that has roughly tripled in value as we have been informed from just a year ago.

There is one big caveat though. Depending on how you look at it, Bitcoin has been the best inflation hedge around. Over the last decade, the headline CPI figure has risen roughly 28 per cent, and denominating that gauge in Bitcoin shows deflation of 99.996 per cent simply because Bitcoin has appreciated over a million per cent during this period. But let us get back down to earth because the second best inflation hedge would have been Tesla’s stock price.

We happen to be in the “Yeah, my house went up 25 per cent in value, but my favourite restaurant now charges 25 per cent more and I can’t eat my house” camp. So we decided to make sense of it for posterity being not old enough to remember any of the major inflationary periods in history, because the confluence of factors from both demand and supply side will make this period an excellent case study in the future.

From the cost side, we can break it down into three broad categories; namely wages, raw materials and logistical disruptions while from the demand side, we would broadly attribute to pent-up demand due to the lockdowns, revenge spending and ESG initiatives.

Everything is happening all at once from the lack of workers to the port log jams to soaring commodities, and it is virtually impossible to pinpoint how it started except that we began blaming the pent-up demand from the series of economic lockdowns around the world, which led to a supply chain shock in the early days—earlier this year and dismissed it all as transitory.

Wages are rising in general and for several reasons. The transitory reason would be border closures preventing low-cost migrants to Singapore and the US, etc. and we hear of staff shortages in Singapore leading to workplace walkouts when one cook does the job of three. In Australia, the UK and US, fruit harvests went to waste due to the lack of seasonal workers.

The more “sticky” wage increases would be the rise in minimum wages around the world as populist policies address wealth gaps and it is happening right here in Singapore when we read about monthly wages for security officers to double over a 6 year period from 2023, which will undoubtedly filter through somehow into our hawker prices and into the economy. Big Mac inflation has started in America as menu prices were raised last month on worker wages.

Even if we assume that automation and productivity improvements will eventually reduce the demand for workers, we should remain cognisant that population demographics for much of the developed world is skewed towards massively ageing and retiring populations and declining working-age populations, with even bigger declines to come as birth rates keel over around the world with a neurotic Gen Z less inclined on marriage and babies. Or even working as it is estimated almost 1 in 5 young adults (3.8 million) in the US is neither working nor studying.

Yes, cryptos come to mind as it is reported that 4 per cent of Americans have quit their jobs due to crypto gains and that is before the run-up while many more are emboldened to play video games for crypto gains as the crypto market capitalisation has swelled to almost $3 trillion, not counting the potential of the rest of the DeFi economy in the upcoming Metaverse.

Finally, it may just as well be that the “lying flat” movement is overtaking the world’s youth. We are not sure but the wage uptrend looks intact with college graduates starting salaries at an all-time-high in the US, especially when Wall Street influencers out-earn bankers. All ready to filter into inflation for a while.

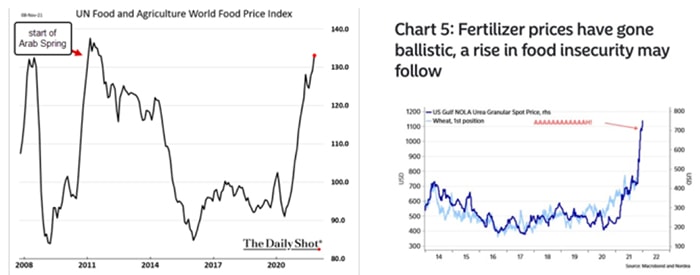

Commodities and raw materials. Let’s start with food and it is not just about the labour shortage for the farmers to slash production. Cost of production has increased with surging fertiliser costs (along with the labour shortage) and weather and logistical disruptions.

Fertiliser prices lead to increases in wheat, corn and soy (animal feed), which feeds into higher prices for meat and dairy. Throw in inclement weather patterns, the drought in Canada that will cut crop production by 26 per cent, rains, floods and rising sea temperatures eating into edible oils, shellfish, fruits, vegetables, cotton and livestock harvests and the labour shortages as well as supply chain disruptions. And let us not forget the diseases like the African swine flu, white striping disease that hit 99 per cent of US supermarket chicken, bird flu, mad cow disease in Brazil, the UK and more.

Demand for metals and commodities has risen as energy costs are rising with the northern hemisphere bracing for a cold winter with some Chinese cities seeing the highest snowfall in 116 years. It has become a threat to the production of metals like magnesium and zinc as US coal miners are sold out for 2022 on the energy crisis, and factories are laid to idle on power outages, raw material and parts shortage.

Transiting to renewable energy sources has led to demand for all the ESG metals like copper (inventories at lowest levels since 2008), lithium and cobalt, driving prices higher and everything else along the way.

We are unable to decide if higher commodity prices are transitory, but Earth does not have an infinite source of oil or coal. Global warming is real so the cost of crop insurance (if there is such a thing) will be going up and we still need to eat real food even if we live in the Metaverse.

Disruptions. It was the port log jam, then the semiconductor chips, then the truckers, the container freight rates and worker shortages. We also have all the government interventions, export bans, lockdowns, sanctions from slave labour for Malaysian gloves and the Xinjiang oppression and more to thank for, which may escalate in the future as short-term fixes.

Luckily, the worst may be over for shipping costs, which have shown signs of trending down and chip shortages are projected to become chip gluts next year.

Our Thoughts

Nonetheless, Krispy Kreme, Johnson and Johnson, P&G, Kraft Heinz, Unilever, Nike, FedEx and many companies, including our friendly neighbourhood Cold Storage, cafes, used car dealers and all, have already proceeded to raise prices. Higher prices are here to stay and it is OK.

The beauty of CPI or inflation is that it is a measure of price increase and prices cannot increase indefinitely, which means it is safe to say that the regulators are right about the transitory bit. We cannot have US CPI rising 6.2 per cent every month. Besides wage rises will offset price increases.

The main people who will be affected are those on fixed incomes, as Federal Reserve’s Williams said on Friday. Like our friend who has to squeeze the extra 0.25 per cent from his portfolio for his electricity expenses or those whose wages are stagnant like many of our friends who are not privileged to wage hikes (and not too heavily invested in crypto, as a joke).

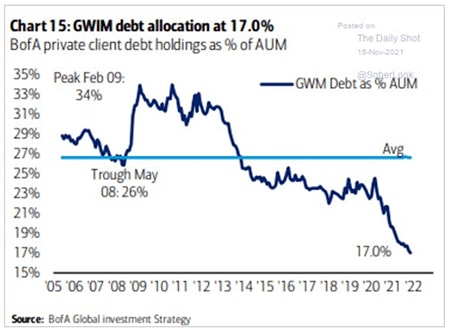

Folks in the markets are already aware of inflationary pressures because inflation breakeven rates are at 16-year highs if not at record highs in places like Germany, disregarding central banks’ rhetoric, as private clients’ portfolio allocation to bonds plummets to lows.

The other worry would be that food insecurity would be politically destabilising, particularly in the less fortunate countries, which also happen to be food producers. And we have the Arab Spring to attest to that and ongoing water protests in Iran, granted that President Biden’s popularity has taken a hit as well.

In the longer term, if such problems are not quickly addressed, we will have a generation of children growing up with nutritional deficiencies and health issues to address, which brings us back to the Band Aid days of famine in Africa.

We have good reason to believe that inflation will continue without worrying about Singapore’s impending GST hike (which is not part of the CPI basket and hence, “not inflationary”) and list the risks below.

– Wage pressures will continue as a function of demographics and migratory policies

– The pivot to ESG will continue to strain bottom lines and sway demand, causing disruptions that will translate ultimately into prices we pay for goods and services

– Weather patterns will continue to disrupt raw material and commodity production and supply chains

– Politics and populist policies like President Biden’s $1 trillion spending plan will boost energy-intensive and material-consuming industries to create challenges in terms of inflation and supply shortages.

The wagers are off—if the ECB’s warnings of asset market corrections trigger a global slowdown and all that comes with it, which we will not bother to expound here. And what to invest in? A story for another day. We have nothing but inflation on our minds for now because that electricity bill will be filtering into our lives.